Gold IRA Company Red Flags: What to Avoid

Gold is trading above $4,600 an ounce as I write this. That's not a coincidence — it reflects genuine investor anxiety about inflation, currency debasement, and the long-term reliability of paper assets. I've held gold and silver inside a self-directed IRA for over a decade, and I understand the appeal of getting some of your retirement wealth out of the financial system and into something tangible.

But here's what I've also watched over 15 years: the exact same conditions that drive legitimate interest in gold also attract the worst operators in the financial industry. When gold prices rise and retirement investors are anxious, predatory gold IRA companies sharpen their pitches. The CFTC has called precious metals fraud particularly damaging to people near retirement — those who cannot afford to re-enter the workforce if something goes wrong. The SEC has taken enforcement action against gold dealers marking up metals by 130% over spot price. State attorneys general have recovered millions from investors who lost their savings to operators who were technically "selling gold" but were functionally running confidence schemes.

The good news is that gold IRA company red flags are learnable. Every predatory tactic in this industry follows a recognizable pattern. This article is the guide I wish I'd had when I first started looking at precious metals for my own retirement. I'll walk through each major warning sign in detail, explain why it matters, and tell you exactly what to do instead.

Why the Gold IRA Industry Attracts Bad Actors

Before we get into specific gold IRA company red flags, it's worth understanding the structural reasons why this industry is particularly vulnerable to predatory behavior.

First, transactions are large. A gold IRA rollover typically involves $25,000 to $500,000 or more — amounts large enough that even a modest percentage overcharge translates into thousands of dollars of real money flowing from your pocket to the dealer's. Second, the product is genuinely confusing. A gold IRA involves at least three separate entities — the dealer, the IRA custodian, and the depository — plus IRS regulations most investors have never encountered before. Complexity is the friend of the bad actor. Third, the target demographic is emotionally primed. Retirement investors worried about inflation and market instability are precisely the people most susceptible to fear-based messaging. Any salesperson who tells you "the dollar is about to collapse and gold is the only protection" is exploiting that vulnerability deliberately.

None of this means gold IRAs are inherently unsafe. The legitimate companies in this space are listed below:

These companies, along with a handful of others, have collectively served hundreds of thousands of investors responsibly. But the existence of good actors doesn't mean you can skip due diligence. The gold IRA company red flags below are real, documented, and currently in use by operators who are targeting retirement investors right now.

Red Flag #1: High-Pressure Sales Tactics and Artificial Urgency

This is the single most reliable signal that you're dealing with a company that does not have your interests at heart.

Legitimate gold IRA companies encourage you to take your time, consult a financial advisor, and ask as many questions as you need. They know that an investor who fully understands the product makes a better long-term client. Companies that need to close you fast are companies that can't afford to let you think.

The pressure tactics you'll encounter sound like this: "Gold prices could spike this week — if you wait you'll miss this entry point." "We can only hold this allocation for 24 hours." "I need to know today before the markets open tomorrow." "Call volume is extremely high right now and I need to get your paperwork started."

None of these statements reflect any real urgency. Gold prices don't disappear. There is no allocation being held for you. These are closing techniques borrowed from the worst traditions of high-pressure sales, and they have no place in a transaction involving your retirement savings. Any gold IRA company that calls you multiple times per day after an initial inquiry, or that creates artificial scarcity around a standard IRA rollover, is showing you a red flag in real time.

My rule: give yourself a minimum of one week between your first call with any gold IRA company and funding any account. A legitimate company will still be there in a week. They'll still have the same products at comparable prices. If a company tries to convince you that isn't true, walk away.

Red Flag #2: Refusing to Put Fees in Writing

Fee opacity is the second most common gold IRA company red flag, and in some ways it's more financially damaging than high-pressure sales, because it can persist undetected for years.

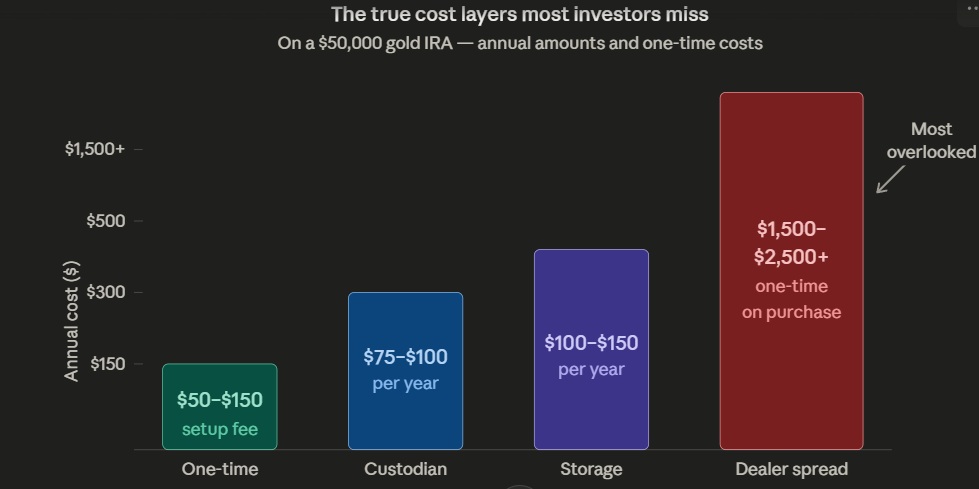

A reputable gold IRA company will provide you with a complete, written fee schedule before you commit — not after, not during the paperwork process, not buried in the fine print of a custodian agreement you're expected to sign under time pressure. The written schedule should cover: one-time account setup fees, annual IRA custodian fees, annual storage fees (with separate pricing for segregated vs. commingled storage), any wire transfer fees, any account closing fees, and any distribution fees when you eventually take possession of or sell your metals.

What you'll find with problematic companies is that fees are quoted verbally — and verbal quotes are impossible to hold anyone accountable to. You'll also find "fee schedules" that list custodian and storage costs but omit the dealer's spread on the actual metals you purchase. This is deliberate. The annual custodian fee of $75–$100 sounds reasonable. The storage fee of $100–$150 sounds reasonable. What doesn't get disclosed is that on a $50,000 metals purchase, you might be paying a 10–20% dealer markup — representing $5,000 to $10,000 that leaves your account on day one, before the metals even arrive at the depository.

Ask for everything in writing. If a company hedges — "our fees vary, I'd have to look that up, we'll include that in the account documents" — treat that as a warning sign. You should know your complete cost before you move a single dollar.

Red Flag #3: Promoting Home Storage Gold IRAs

If a company suggests you can store your IRA-owned gold at your home — sometimes framed as a "home storage IRA," a "checkbook IRA," or an LLC-based arrangement — stop the conversation immediately.

The IRS position on this is not ambiguous. IRA-owned metals must be held by an approved custodian and stored at an IRS-approved depository. Period. The Tax Court has ruled repeatedly against investors who attempted home storage arrangements — in the landmark McNulty case, the court found that keeping metals at home constituted a taxable distribution, triggering income taxes plus a 10% early withdrawal penalty on the entire IRA balance. The IRS has an active consumer alert specifically warning investors about companies promoting home storage gold IRAs, noting that they frequently misrepresent the legal basis for these arrangements.

Any company that promotes home storage for IRA metals is either dangerously uninformed about tax law or deliberately misleading you. In either case, the financial consequences you would face — not the company — if the IRS challenges your account. Your entire retirement balance could be at risk.

The appropriate setup is simple: your metals are purchased for your IRA, held by a registered custodian, and stored at an approved depository such as the Delaware Depository or Brinks Global Services. You don't have physical access to the metals during the IRA's active period — that's the tradeoff for the tax advantages. Any pitch that promises you both the tax benefits and personal possession of your metals is not describing something that exists legally.

Red Flag #4: Steering You Toward Numismatic or Collectible Coins

This is one of the most financially destructive gold IRA company red flags, because it often goes undetected for years and can dramatically reduce your effective return.

Standard IRA-eligible gold — American Gold Eagles, Canadian Maple Leafs, American Buffalos, and bars from accredited refiners — typically carries a dealer markup of 3–8% above spot price. That's the normal cost of doing business in this market. Numismatic or "collectible" coins — graded proof coins, rare mintage issues, "semi-numismatic" coins — can carry markups of 30%, 50%, or even 130% or more above spot. The SEC's action against Red Rock Secured documented markups in that range, with investors being told they were receiving special, high-value coins when they were simply paying far above market for the gold content.

The pitch sounds like this: "These proof coins have collector value above and beyond their gold content, so they appreciate faster." "These coins are considered non-reportable, which protects you from government confiscation." The confiscation narrative is historically based on the 1933 Executive Order 6102 — a law that has been repealed and that explicitly exempted coins with numismatic value even when it was active. It is scare-marketing, not financial analysis.

Within an IRA, you don't benefit from numismatic collector value the way you would holding coins directly. Your IRA is a retirement account, not a coin collection. The premium you pay for collectible status is effectively dead weight — you're paying more per ounce of gold without any proportional increase in the underlying metal you own. Stick to standard bullion products. If a representative pushes back on that preference or implies you're making a mistake by not upgrading to premium coins, that is a direct red flag.

Red Flag #5: Claiming Guaranteed Returns

Any gold IRA company that implies or states your investment is guaranteed to grow — that gold "always goes up," that it's "risk-free protection," or that a gold IRA guarantees your retirement wealth — is making a claim that is both factually false and a securities violation.

Gold has performed well during specific periods of economic stress. It rose significantly during the 2008 financial crisis, surged during the COVID panic, and has climbed sharply through the current period of inflation and monetary uncertainty. I hold it in my own IRA specifically because of its behavior during these kinds of periods. But gold can also trade sideways for years. It can decline substantially in nominal terms. It is not a bond with a stated return. It is a commodity whose price reflects the intersection of global demand, monetary policy, currency dynamics, and investor psychology.

A company that tells you otherwise is either incompetent or deliberately misleading you to close a sale. Neither is a company you want holding your retirement assets. Look for companies that present gold honestly — as a long-term diversifier and store of value, with real risks alongside the potential benefits. That kind of honesty is a positive signal. Its absence is a red flag.

Red Flag #6: Unverifiable Ratings and Fake Social Proof

Many gold IRA company red flags are easy to spot once you know what to look for — but fabricated social proof requires a small amount of active verification to catch.

Here's what legitimate credentialing looks like: an A+ rating from the Better Business Bureau means the company is accredited, has a certain operating history, and has resolved complaints in the BBB's view. An AAA rating from the Business Consumer Alliance is a meaningful independent signal. Trustpilot ratings from thousands of verified reviews over multiple years represent genuine customer sentiment.

Here's what fabricated credentialing looks like: "Best Gold IRA Company" badges from an organization you've never heard of that the company itself sponsors. Industry award logos without any verifiable issuing body. Five-star ratings on a review platform you can't independently access. Testimonials from unnamed customers with no verifiable details.

Before trusting any rating or award on a gold IRA company's website, verify it directly at the source. Go to bbb.org and look up the company yourself — not the link on their website, but the independent search. Check Trustpilot and Google Reviews directly. Look at the Business Consumer Alliance at trustbca.org. Pay particular attention to the pattern of complaints — a company with 1,200 reviews and six unresolved complaints looks very different from a company with 200 reviews and 15 unresolved complaints.

Red Flag #7: Hidden Dealer Spreads and Promotional Traps

Understanding the difference between advertised fees and total cost is perhaps the most important piece of financial literacy for any gold IRA investor. It's also an area where even well-intentioned investors get caught.

The annual custodian fee ($75–$100) and storage fee ($100–$150) are real costs, but they're also the most visible and competitive part of the pricing structure. The cost that actually separates good dealers from predatory ones is the premium above spot price — what you pay for the metal versus what the metal is worth on the open market at the moment of purchase. A 3% premium on a $50,000 purchase means $1,500 leaves your account on day one. A 10% premium means $5,000. A 30% premium means $15,000.

"Free silver" and "bonus metals" promotions deserve special scrutiny. A company that offers you $5,000 in free silver when you open an account is not giving you anything for free. The cost of that promotional silver is almost certainly embedded in the premiums on the metals you purchase. Before accepting any promotional offer, compare the pricing on the specific gold or silver products you're buying against at least one other dealer quoting on the same items. If the premium is higher with the promo company, the promotion is costing you money, not saving it.

The CFTC has warned that spreads in the precious metals industry can range from 30% to 300% or more with fraudulent operators. The SEC has documented cases of retirees paying $1.30 for every dollar of gold they received. These are extreme cases — but they illustrate the mechanism. Your protection is not trusting a company's marketing. Your protection is a written itemized quote on specific products, compared against the current spot price, before you fund.

Red Flag #8: Leveraged or Financed Account Structures

This is a less common red flag but a particularly dangerous one. Some gold IRA operators have allowed or encouraged investors to make purchases with as little as 20–25% down, financing the remaining 75–80% of the metals purchase.

Leveraged precious metals accounts are not gold IRAs — they are speculative instruments with all of the downside risk of leverage and none of the tax protection of an IRA structure. In some documented cases, investors believed they owned gold outright inside a retirement account when they were actually holding a leveraged commodity position with significant risk of total loss.

If any gold IRA company mentions financing, leverage, margin, or "buying more gold than your deposit allows," terminate the conversation. A legitimate gold IRA involves purchasing metals outright with funds already in your retirement account. There is no legitimate financing component.

Red Flag #9: No Verifiable Operating History or BBB Record

Operating history matters in this industry for a specific reason: the rollover process, the custodian relationships, and the depository arrangements all involve ongoing coordination that takes years to execute consistently. A company that has been operating for 10 or 20 years and maintained A+ BBB ratings throughout has been tested in real market conditions — the 2008 crash, the 2020 collapse, the inflation surge of the early 2020s. A company founded 18 months ago has not.

This doesn't mean newer companies are automatically suspect. American Hartford Gold was founded in 2015 and has built a genuinely strong reputation. But any company that can't point to a multi-year BBB record with a consistent pattern of resolved complaints should be approached with extra caution.

Pay particular attention to the nature of complaints even at highly-rated companies. Unresolved complaints around delivery delays, fee disputes, or difficulty liquidating are more concerning than complaints about communication preferences. A pattern of investors struggling to get their metals out of a company — whether through difficulty selling or unexplained processing delays — is a warning sign regardless of the overall rating.

A Framework for Evaluating Any Gold IRA Company

After 15 years in this market, here is the process I apply before recommending or engaging any gold IRA company:

Step 1: Verify ratings independently. Look up the company directly at bbb.org, trustbca.org, Trustpilot, and Google Reviews. Note the number of reviews, the rating, and — critically — the unresolved complaint rate.

Step 2: Request everything in writing. Ask for a complete, itemized fee schedule covering setup, annual custodian, annual storage (segregated and commingled), wire fees, distribution fees, and account closing fees. If they won't send it in writing, stop.

Step 3: Get a product quote. Ask for a written price on specific IRA-eligible bullion products — for example, a 1 oz American Gold Eagle and a 1 oz Gold Buffalo. Note the premium above the current spot price. Compare that same quote with at least one other dealer on the same day.

Step 4: Ask about the buyback process. How is the buyback price determined? What benchmark is used? What is the typical spread between purchase price and buyback price? How long does the process take? Get the answers in writing.

Step 5: Confirm the custodian and depository. Who will hold your IRA? Who will store your metals? Verify that both are IRS-approved. Confirm whether your storage will be segregated or commingled, and whether you can change that preference.

Step 6: Take a week. Don't fund anything for at least a week after your first conversation. Use that time to do your own research, check independent review sites, and consult a licensed financial advisor if your situation warrants it.

What a Trustworthy Gold IRA Company Looks Like

For contrast, here's what the absence of red flags looks like in practice.

A trustworthy gold IRA company publishes its fee structure or provides it immediately in writing when asked. It presents gold and silver as one component of a diversified retirement strategy, not as a solution to every financial problem. It gives you time and encourages you to ask questions. It steers you toward standard IRA-eligible bullion and can explain clearly why collectible coins are not in your interest. It maintains a multi-year BBB record with a low unresolved complaint rate. It confirms, proactively, that your metals will be stored at an approved depository and never suggests home storage as an option.

The companies I trust in this space — and I've mentioned them in detail in other articles on this site — are transparent about costs, patient with customers, and willing to turn away business that isn't a good fit. That last quality is perhaps the most telling of all. A company that tells you gold might not be right for your situation is a company confident enough in its model to prioritize your outcome over its commission. That's exactly the kind of partner you want when you're deciding where to put your retirement savings.

The Bottom Line on Gold IRA Company Red Flags

The precious metals industry has genuinely improved its standards over the past decade. The top companies today are more transparent, better regulated, and more accountable than they were when I first started in this space. But the incentive structures that have historically produced bad actors haven't disappeared — large transaction sizes, a complex product, and emotionally primed buyers will always attract operators willing to exploit those conditions.

Knowing the gold IRA company red flags detailed in this article won't just protect you from outright fraud. It will also protect you from the far more common scenario: a technically legitimate company that quietly overcharges you on premiums, pushes you into inappropriate coins, or buries fee structures that compound quietly over years.

The gold IRA process is not complicated when you work with the right company. It's a straightforward rollover into a self-directed account, metals purchased at transparent prices, stored at a reputable depository, with clear annual costs and a reliable buyback program. That's it. If any part of the experience is being made to feel more urgent, more complex, or harder to verify than that description suggests, you're probably looking at a red flag.

Take your time. Get it in writing. Compare quotes. And trust the process more than the pitch.